The senior editor refreshed the dashboard one more time. Her team had spent eight months on the savings-account guide. Three months on the home-loan comparison. The reads were up. The reads were way up. The clickthroughs were not. The referrer breakdown explained the gap: ChatGPT, Claude, Perplexity, Gemini. Agents reading her team’s analysis at industrial scale, then routing the buyers somewhere else.

She’d been promoted six years ago to grow the comparison brand. She’d done it. Trust at all-time highs. Content read volume at all-time highs. AI referrer traffic at all-time highs. The single metric that paid the bills – affiliate revenue per visitor – was in structural decline. The line was getting steeper every quarter.

This is the second discovery of the buyer-agent era. The first is what happens to your own funnel. The second is what happens to the businesses that have spent twenty years living between funnels.

The aggregator-comparison-affiliate layer of the internet existed because buying was hard. Buyer agents make buying easy. The whole middle layer – comparison sites, affiliate review brands, lead-gen brokers, rate aggregators, listing platforms – is about to find that the function it sold has been absorbed by the platforms its customers now talk to first. This isn’t a slow decline. The mechanism is structural, and once buyers stop visiting, no amount of SEO recovers what’s gone.

If your business gets demand through aggregators, that channel is weakening. If your business pays aggregators for placement, that spend is buying borrowed time. If your business is an aggregator, you have a strategy memo to write, and you don’t have years.

Aggregation, comparison, filtering — gone

Compare the Market existed because no buyer could query forty insurance providers in an afternoon. Skyscanner existed because no buyer could pull live fares from a hundred airlines. Trivago existed because hotel pricing was a maze of opaque conditions. iSelect existed because nobody had time to read forty utility plans. Realestate.com.au existed because residential listings sat in MLS systems that didn’t speak to consumers. The whole category was built on a single buyer constraint – the inability to compare options at scale.

Buyer agents resolve that constraint in milliseconds. An agent told to find the cheapest comprehensive car insurance for a thirty-five-year-old in Sydney with a clean driving record will query the same primary sources Compare the Market queries, apply more variables than Compare the Market can capture, factor in the buyer’s history and preferences, and route directly to whichever insurer wins. The aggregator is not in the path.

This is not future tense. At Google I/O 2026 on 19 May, Google announced that information agents inside Search will now do exactly this for apartment hunting – a buyer brain-dumps their requirements and the agent continuously scans the web for listings that match, notifying the buyer when something lands. The functions that built Realestate.com.au, Domain, and every property aggregator on the internet just became default features of the search box one billion people already use. The aggregator’s distinct surface stops being necessary.

The same logic flattens flight comparison, hotel comparison, utility comparison, broadband comparison, credit card comparison, mortgage comparison, listing platforms in residential real estate, lead-gen brokers in finance and home services, and the unbranded long tail of niche compare-everything sites that earn through display ads and lead fees. Wherever the business model was we collected the options for you, the buyer no longer needs them collected. The agent does the collecting on the buyer’s side, personalised in ways no public site could match.

This is the cleanest function-loss in the agent economy. There’s no editorial moat, no brand permission, no premium-tier escape. The work itself has been replaced.

Aggregation

ReplacedAI consolidates content sources, no human aggregation needed.

Comparison

ReplacedAI agents instantly compare features, prices, specs.

Filtering

ReplacedUser-specific context removes need for manual filters.

Affiliate monetisation

TerminalAI answers directly, bypassing revenue-driving links.

Editorial judgment

Brand survivesUnique, high-value insights from human experience remain.

Trust verification

Brand persistsVerified reputation and accuracy become key differentiators.

Survives

Vertical expertise

Deep, niche knowledge and specialized human insight remain essential and highly valuable.

The affiliate model breaks, even where the content is good

The harder discovery – and the one editorial teams haven’t fully metabolised yet – is that the affiliate revenue model depends on a specific buyer behaviour that agents simply don’t perform.

Buyers used to read a recommendation, click a tracked link, and arrive at the seller through the recommender’s affiliate code. The recommender got paid. Everyone agreed this was the system. Twenty years of internet content — review sites, financial guides, “best of” lists, product comparisons, deal sites, and most of consumer SEO – was funded by this single mechanism.

Agents read recommendations as input data and route the buyer directly. There’s no click. There’s no affiliate code. The seller gets the sale. The recommender gets nothing. Google’s I/O 2026 announcement put the mechanism into product roadmap form: information agents now scan blogs, news sites, and social posts continuously, synthesising findings for the user. The editorial work is consumed at scale; the click that paid for it is replaced by the synthesis.

Wirecutter, NerdWallet, MoneySavingExpert, ProductReview, and tens of thousands of smaller editorial-affiliate sites all run on this single rail. The rail is being engineered out of the buying process by every major agent platform. The content keeps getting written. It keeps getting consumed. It keeps getting cited. The revenue stops following.

You can already see the early signal in affiliate-network reporting. Generative-platform referrals are climbing fast in raw volume while conversion-to-sale through affiliate codes is plateauing or falling. The two lines diverging is the mathematical signature of the problem: read at scale, monetise at zero.

The exception that isn't

You might be reading this thinking the strong editorial brands are protected. Wirecutter has fifteen years of independent testing. NerdWallet has real financial analysts. MoneySavingExpert has Martin Lewis and a national reputation. These aren’t aggregators – they’re judges. Surely the judgment survives.

The judgment does survive. The brands persist. Trust earned over a decade doesn’t evaporate because the platform layer changed. What evaporates is the business model that funded the judgment.

Wirecutter’s recommendations become input data for ChatGPT, which routes the buyer to Amazon, which pays a commission to nobody at Wirecutter. The trust persists; the revenue doesn’t, because the revenue was always conditional on clickthrough and clickthrough is the thing the agent removes.

The new customer for editorial judgment isn’t the buyer. It’s the agent. And the agent doesn’t pay for content the way buyers used to pay through clicks. Editorial brands are about to discover that they spent a generation building authority that’s now being inherited, royalty-free, by the agent platforms.

Some will pivot – direct subscriptions, licensing deals with agent platforms, advisory services sold to sellers, rebuilding around vertical expertise that agents can’t synthesise on the fly. Most will find that the pivot is harder than running the original model and the timeline is shorter than the runway suggests. The brand will be intact when the lights go out.

What survives, and where the value actually goes

The piece of the middle layer that does survive is vertical expertise so specific that the analysis itself is the product – not aggregation, not affiliate. Specialised legal advice for complex situations. Tax guidance for unusual cases. Medical second-opinion services. Forensic financial analysis. Bespoke creative direction. Anywhere the work is interpretation rather than collection, the human or specialised system that performs the interpretation keeps its value, because the buyer can’t fully specify the question to an agent without first engaging with someone who can frame it.

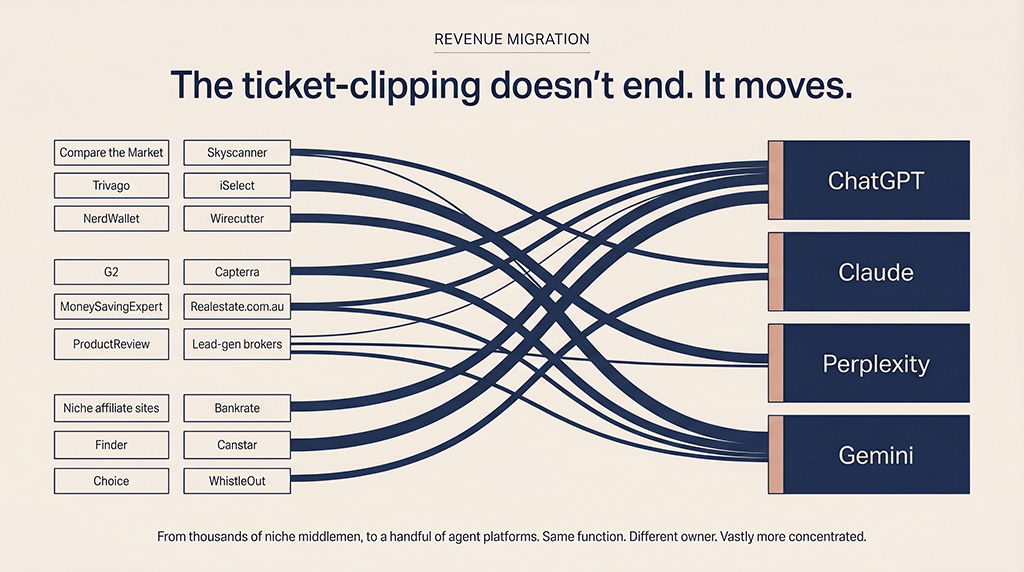

Everything else consolidates upward. The functions the aggregators sold – collect, compare, filter, recommend, route – don’t disappear. They get absorbed by ChatGPT, Claude, Perplexity, Gemini, and whichever agent platforms last the decade. The ticket-clipping doesn’t end. It moves. From thousands of niche middlemen taking five to thirty percent of various transactions, to a handful of agent platforms taking whatever cut they decide their position is worth, with vastly more concentrated power.

This is the macroeconomic shape of the next two to three years: a vast layer of internet revenue, currently distributed across compare/review/aggregate/affiliate businesses, getting pulled into the agent platforms themselves. The middle layer of the internet, where so much of the last twenty years of revenue accrued, is becoming a thinner layer with new owners.

For the SMB audience, two practical reads. If you currently get demand through aggregators – bookings, leads, listings, comparison rankings, B2B software through G2 or Capterra – that channel is on a clock. Don’t let it become a single point of failure. Reorient toward agent-readable presence on your own surface, which is the work the buyer agent audit identifies. If you currently pay aggregators for placement – affiliate fees, lead costs, commission splits — don’t double down. The placement gets you in front of fewer buyers every quarter. Reinvest in the layers buyer agents actually read.

The editor in Sydney started a new document at the end of the quarter. Her first heading: What is a comparison site, when buyers have stopped comparing? She didn’t have an answer. None of her competitors did either. The trust they’d spent fifteen years building was intact. The business model that had funded it wasn’t. Her strategy memo would have to acknowledge what the dashboard had been telling her all year, in numbers her office had been quietly trying not to read.

The disintermediators are about to be disintermediated by exactly the technology that lets buyers do directly what aggregators once did for them. Most won’t survive the consolidation in the form they’re in now. Some will pivot. A few will rebuild around the slim band of analysis the agent can’t replace. Everyone in the middle has the same memo to write, and the only question that matters is how many quarters they get to write it in.

Find out which of your channels are about to be skipped

Most SMBs we audit have channel mixes that lean heavily on aggregator-driven demand – bookings via Trivago, leads via iSelect, listings via Realestate.com.au, B2B trials via G2 – without realising the channel is on borrowed time. More placements. Higher fees. Flat conversion. We’ll show you how exposed your demand actually is and what to build instead.

Takes 30 minutes.